Housing And Civil Enforcement Cases Documents

IN THE UNITED STATES DISTRICT COURT FOR

THE EASTERN DISTRICT OF MICHIGAN

SOUTHERN DIVISION

UNITED STATES OF AMERICA,

Plaintiff,

v.

OLD KENT FINANCIAL CORPORATION

AND OLD KENT BANK,

through their Successors

in Interest,

Defendants.

___________________________________

COMPLAINT

The United States alleges:

Jurisdiction and Venue

1. The United States brings this action to enforce Title VIII of the Civil Rights Act of 1968 ("Fair Housing Act"), as amended by the Fair Housing Amendments Act of 1988, 42 U.S.C. §§ 3601-3619, and the Equal Credit Opportunity Act ("ECOA"), 15 U.S.C. §§ 1691-1691f.

2. This Court has jurisdiction of this action pursuant to 28 U.S.C. § 1345, 42 U.S.C. § 3614, and 15 U.S.C. § 1691(h), and venue is appropriate pursuant to 28 U.S.C. § 1391(c).

Parties

3. Defendant Old Kent Financial Corporation was a bank holding company, which was incorporated under the laws of Michigan in 1984 and was headquartered in Grand Rapids, Michigan, prior to its acquisition by Fifth Third.

4. Defendant Old Kent Bank was a wholly owned subsidiary and principal asset of Old Kent Financial Corporation.

5. Fifth Third acquired Old Kent Financial Corporation and Old Kent Bank through an acquisition approved by the Federal Reserve Board on March 12, 2001.

6. Fifth Third merged Old Kent Bank into First Third Bank (Michigan) as a result of the acquisition of Old Kent Financial Corporation by Fifth Third. The Federal Reserve Board approved this merger on May 14,2001.

7. Fifth Third and Fifth Third Bank are successors in interest to all assets and liabilities of Old Kent Financial Corporation and Old Kent Bank that were procured as a result of the acquisition and the merger described above.

8. Prior to its acquisition by Fifth Third, Old Kent Bank offered the traditional services of a financial depository institution, including the receipt and maintenance of monetary deposits, and the financing of residential, commercial and consumer loans. Old Kent Bank was established in 1853, was incorporated under the laws of Michigan and had its principal place of business in Grand Rapids, Michigan.

9. At the time of the acquisition by Fifth Third, Old Kent Financial Corporation and Old Kent Bank conducted banking business primarily in Michigan, Illinois and Indiana.

10. At the time of the acquisition by Fifth Third, Old Kent Financial Corporation and Old Kent Bank were under the regulatory supervision of the Federal Reserve Board. Fifth Third and Fifth Third Bank currently are regulated by the Federal Reserve Board.

11. As of December 31, 2000, Old Kent Financial Corporation estimated its total assets at $23.9 billion, with Old Kent Bank maintaining an estimated $23.5 billion of those assets.

12. Fifth Third and Fifth Third Bank are, and Old Kent Financial Corporation and Old Kent Bank were, subject to the federal laws governing fair lending including the Fair Housing Act, the Equal Credit Opportunity Act and the Community Reinvestment Act, 12 U.S.C. §§2901-2906. The Fair Housing Act and the Equal Credit Opportunity Act prohibit financial institutions from discriminating on the basis of, inter alia, race, color, or national origin in their lending practices. The Community Reinvestment Act and its implementing regulations impose on banks a responsibility to meet the credit needs of the entire community which they serve, including the credit needs of low to moderate income neighborhoods.

13. Detroit Metropolitan Statistical Area (hereinafter "Detroit MSA"), as designated by the Office of Management and Budget, contains the six Michigan counties of Wayne, Oakland, Macomb, Lapeer, St. Clair and Monroe. These counties are located in the lower southeast corner of the state. The City of Detroit lies within Wayne County.

14. Demographic data compiled by the U.S. Census for the year 2000 show that the African American population of the City of Detroit is over 81% while the African American population of the Detroit MSA - of which the City of Detroit is a part - is approximately 23%. The U.S. Census data reflects the racial segregation in the population, with the majority of the African American population residing in the City of Detroit and the majority of non-African American population residing in the surrounding suburban areas. In the most recent U.S. Census Residential Segregation Index, the Detroit MSA is identified as one of the two most racially segregated MSAs in the United States. See Map attached as Exhibit 1.

{kind=link}

15. Prior to 1995, Old Kent Financial Corporation maintained a corporate structure that included numerous subsidiary banks, including Old Kent Bank. In 1995, Old Kent Financial Corporation consolidated its subsidiary banks into a single bank, Old Kent Bank, which operated out of Grand Rapids, Michigan.

16. Since Old Kent Bank first began operation, it has expanded its business, including that of extending credit for small business loans and residential real estate-related transactions, to substantial portions of the Detroit MSA. Old Kent Bank has engaged in a race-based pattern of locating or acquiring new offices. It has located or acquired new branch and other offices to serve the residential lending and credit needs of predominantly white areas but not those of predominantly African American neighborhoods.

17. As of January 1996, Old Kent Bank operated at least 18 branches in the Detroit MSA. Not a single one of these branches was located in the City of Detroit. As of March 2000, Old Kent Bank had expanded its business presence in the Detroit MSA to include a branch network of at least 53 branches, located in every county of the Detroit MSA. Virtually all of Old Kent Bank's branches were located in predominantly white suburbs. As of March 2000, Old Kent Bank still did not have a single branch in the City of Detroit, where the population is more than 81% African American. See Map attached as Exhibit 2.

{kind=link}

18. In March 2000, the United States notified Old Kent Bank of its investigation into Old Kent Bank's lending practices. Approximately six months after receiving the notice of investigation letter, Old Kent Bank opened a branch in the City of Detroit.

19. In operating and extending the scope of its business, Old Kent Bank has acted to meet the lending and credit needs of predominantly white residential areas (census tracts with a population greater than 50% non-Hispanic white) throughout the Detroit MSA, including Wayne County, and has avoided serving the lending and credit needs of majority African American neighborhoods, which are located almost exclusively in the City of Detroit.

20. Old Kent Bank claims that, prior to 2000, it did not do business in the City of Detroit because it did not have any branches there. Old Kent Bank further claims that it had not opened any branches in the City of Detroit because its policy was to only open or acquire new branches within three miles of existing branches. However, since 1995, Old Kent Bank has repeatedly failed to follow this alleged policy and has opened a number of branches in predominantly white census tracts that were more than three miles from existing branches.

21. Old Kent Bank declined to open branches in the City of Detroit as described above so as to avoid serving that community.

22. Pursuant to the CRA, each covered financial institution must delineate an assessment area defining the geographic region that it reasonably believes it serves. 12 U.S.C. §§2901, et seq., and the implementing regulations promulgated by the FRB, 12 C.F.R. §228, as amended (also known as Regulation BB). Under Regulation BB, a bank's assessment area must consist only of whole geographies, may not reflect illegal discrimination, and may not arbitrarily exclude low or moderate income geographies, taking into account the institution's size and financial condition. Id. at §228.41(e).

23. Instead of defining its assessment area in accordance with Regulation BB, Old Kent Bank circumscribed its lending area in the Detroit MSA to exclude most of the majority African American neighborhoods by excluding the City of Detroit. See Map attached as Exhibit 3.

24. From at least 1996 through 2000, Old Kent Bank has solicited and funded very few small business or residential real estate-related loan applications from predominantly African American census tracts outside its assessment area.

25. From at least 1996 to 2000, Old Kent Bank maintained a policy and/or practice of limiting the contact of its personnel responsible for advertising and soliciting applications for loans with individuals and businesses located in the City of Detroit and/or other majority African American tracts in the Detroit MSA.

26. Analyses of the geographic distribution of the number of originations funded by Old Kent Bank demonstrate that Old Kent Bank has served the credit needs of predominantly white neighborhoods of the Detroit MSA to a significantly greater extent than it has served the credit needs of predominantly African American neighborhoods. Similar analyses of lending activity in Wayne County also demonstrates that Old Kent Bank has served the credit needs of predominantly white neighborhoods to a significantly greater extent than it has served the credit needs of predominantly African American neighborhoods in those geographic areas.

27. Between 1996 and 2000, Old Kent Bank originated 15,423 small business, home improvement, and home refinance loans in the Detroit MSA. Only 335, or 2.2%, of such loans were made in census tracts which were occupied by a majority of African American residents.

28. The U.S. Census reports that in the City of Detroit, over 11,000 (approximately 43%) of the more than 26,000 businesses are owned by African Americans. The 1997 Economic Census also reports that the African American firms in the Detroit MSA generate over $3.5 billion dollars in revenue.

29. Old Kent Bank told African American business owners in the City of Detroit that it would not make business loans in that area and it denied applications for credit from African American owned businesses in the City of Detroit and in African American areas of the Detroit MSA without explanation.

30. In 2000, Old Kent Bank generated 1,977 small business loans in the Detroit MSA, but only 87, or 4.4%, were originated in majority African American census tracts. See Map attached as Exhibit 4.

{kind=link}

31. In 1998, Old Kent Bank generated 1,496 small business loans in the Detroit MSA, but only 20, or 1.3%, were originated in majority African American census tracts. See Map attached as Exhibit 5.

{kind=link}

32. In 1996, Old Kent Bank generated 913 small business loans in the Detroit MSA, but only 19, or 2.1%, were originated in majority African American census tracts. See Map attached as Exhibit 6.

{kind=link}

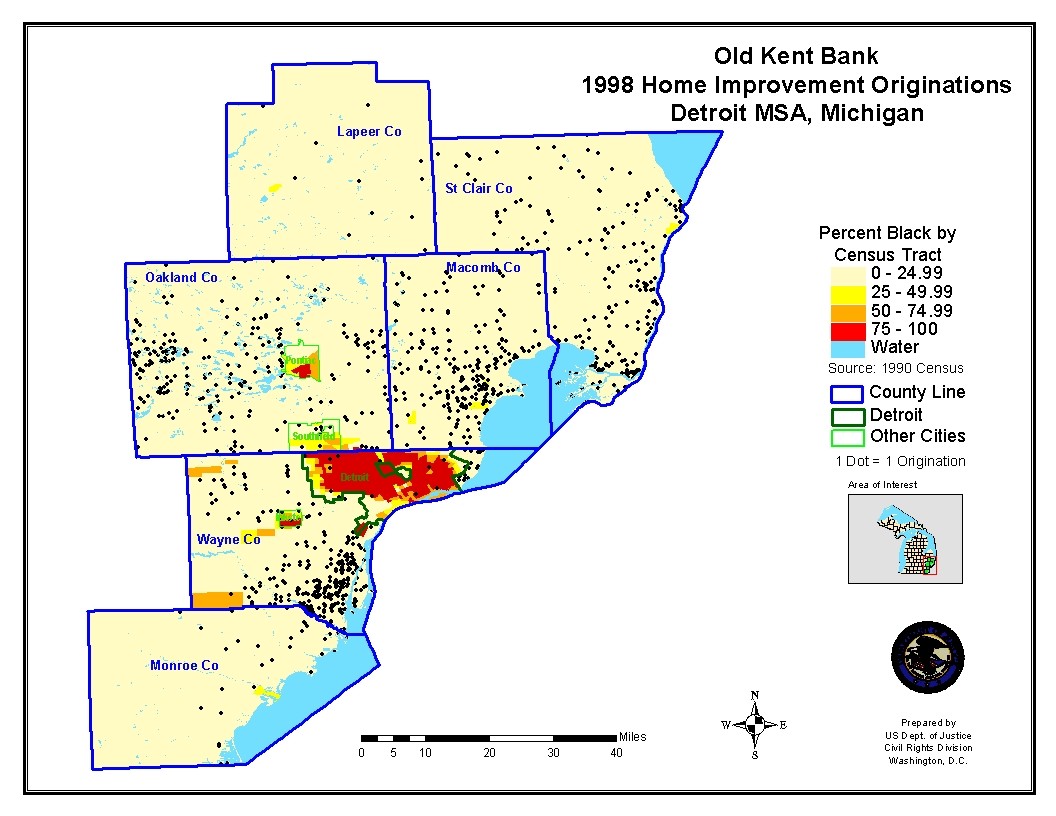

33. In 2000, Old Kent Bank generated 759 home improvement loans in the Detroit MSA, but only 31, or 4.1%, were originated in majority African American census tracts. See Map attached as Exhibit 7.

{kind=link}

34. In 1998, Old Kent Bank generated 1045 home improvement loans in the Detroit MSA, but only 19, or 1.8%, were originated in majority African American census tracts. See Map attached as Exhibit 8.

{kind=link}

35. In 1996, Old Kent Bank generated 715 home improvement loans in the Detroit MSA, but only 14, or 2.0%, were originated in majority African American census tracts. See Map attached as Exhibit 9.

{kind=link}

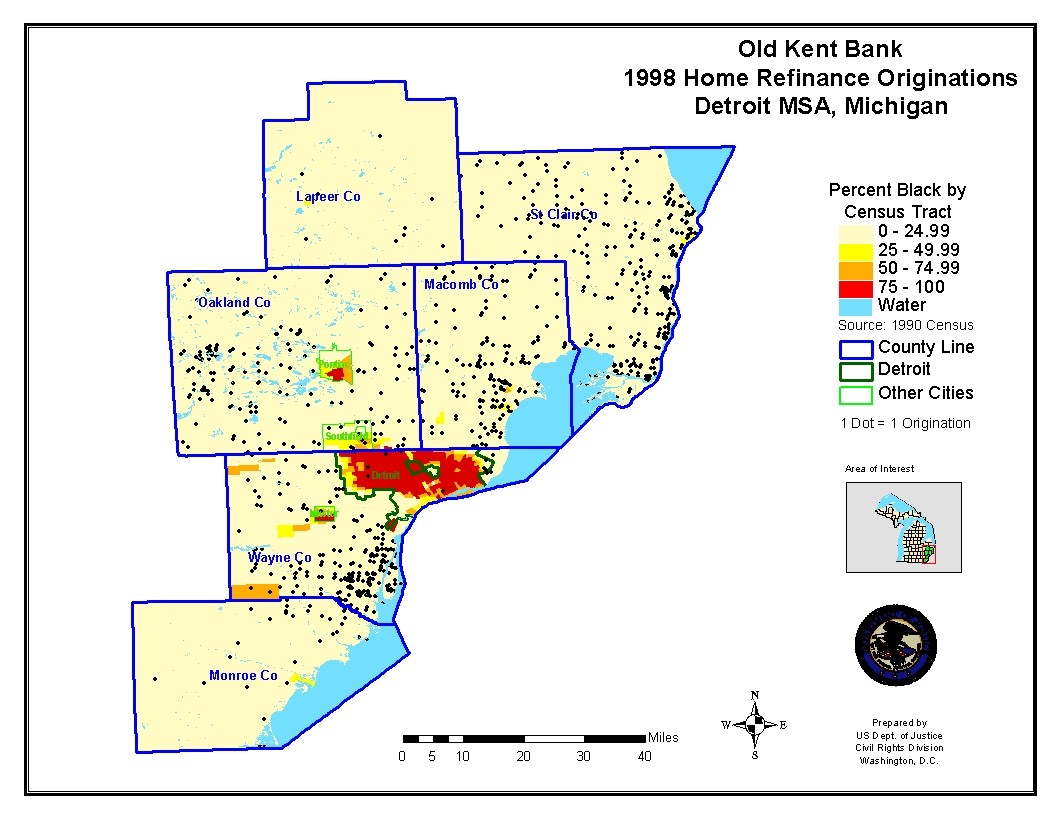

36. In 2000, Old Kent Bank generated 982 home refinance loans in the Detroit MSA, but only 28, or 2.9%, were originated in majority African American census tracts. See Map attached as Exhibit 10.

{kind=link}

37. In 1998, Old Kent Bank generated 857 home refinance loans in the Detroit MSA, but only 10, or 1.2%, were originated in majority African American census tracts. See Map attached as Exhibit 11.

{kind=link}

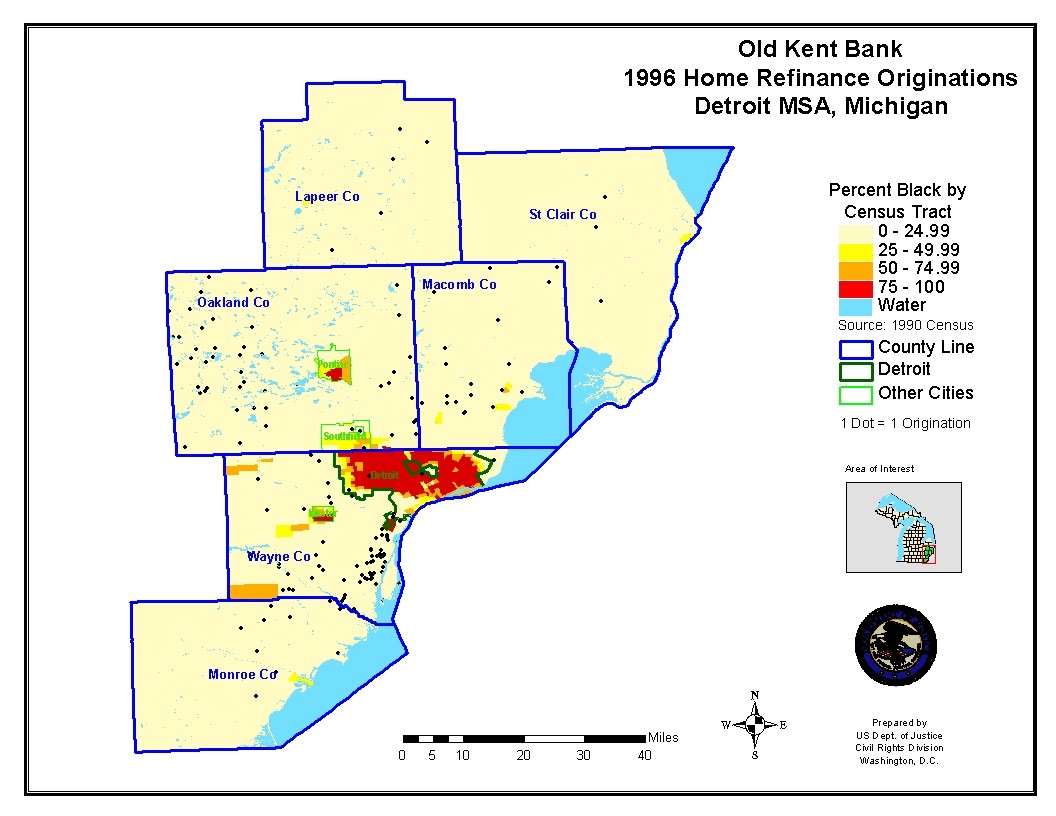

38. In 1996, Old Kent Bank generated 156 home refinance loans in the Detroit MSA, but only 2, or 1.3%, were originated in majority African American census tracts. See Map attached as Exhibit 12.

{kind=link}

39. Unlike Old Kent Bank, many banks and other lenders issued loans to persons or businesses residing in the City of Detroit.

Violations of Law

40. The totality of the defendants' policies and practices described herein constitute the redlining of African American residential neighborhoods of the Detroit MSA thereby severely limiting the defendants' commercial and residential lending business. Their policies and practices deny residents of African American neighborhoods, on account of the racial composition of those neighborhoods, an equal opportunity to obtain credit. These policies and practices are not justified by business necessity or other legitimate, non-discriminatory business considerations. Old Kent Financial Corporation and Old Kent Bank's actions as alleged herein constitute:

- Discrimination on the basis of race and/or color in making available residential real estate-related transactions in violation of the Fair Housing Act, 42 U.S.C. § 3605(a).

- Discrimination against applicants with respect to credit transactions on the basis of race and/or color in violation of the Equal Credit Opportunity Act, 15 U.S.C. § 1691(a)(1).

- A pattern or practice of resistance to the full enjoyment of rights secured by the Fair Housing Act, 42 U.S.C. §§ 3601, et seq.,;

- A denial of rights granted by the Fair Housing Act to a group of persons that raises an issue of general public importance, 42 U.S.C. §§ 3601, et seq.; and

- A pattern or practice of activity in violation of the Equal Credit Opportunity Act, 15 U.S.C. § 1691e(h); and

41. The policies and practices of Old Kent Bank and Old Kent Financial Corporation as alleged herein constitute:

42. Persons who have been victims of Old Kent Bank and Old Kent Financial Corporation's discriminatory policies and practices are aggrieved persons, as defined in 42 U.S.C. § 3602(i), and have suffered damages as a result of Old Kent Bank and Old Kent Financial Corporation's conduct as described herein.

43. Persons who have been victims of Old Kent Bank and Old Kent Financial Corporation's discriminatory policies and practices are aggrieved applicants, as defined in 15. U.S.C. §§ 1691a and 1691e and interpreted through Regulation B, 12 C.F.R. §§ 202, et seq., and have suffered damages as a result of Old Kent Bank and Old Kent Financial Corporation's conduct as described herein.

44. The discriminatory policies and practices of Old Kent Bank and Old Kent Financial Corporation were intentional, willful and implemented with reckless disregard for the rights of African American business owners and home owners and those who are located in majority African American communities throughout the Detroit MSA.

WHEREFORE, the United States prays that the Court enter an ORDER that:

(1) Declares that the policies and practices of Old Kent Bank and Old Kent Financial Corporation constitute violations of the Fair Housing Act, 42 U.S.C. §§ 3601-3619 and the Equal Credit Opportunity Act, 15 U.S.C. §§ 1691-1691f; (2) Enjoins the defendants, their agents, employees and successors, specifically all those previously employed or working as agents of Old Kent Bank and Old Kent Financial Corporation, and all other persons in active concert or participation with them, from:(a) discriminating on the basis of race and/or color in any aspect of their business practices or transactions;

(b) failing or refusing to take such affirmative steps as may be necessary to restore, as nearly as practicable, the victims of the Old Kent Bank and Old Kent Financial Corporation's unlawful practices to the position in which they would have been but for the discriminatory conduct;

(c) failing or refusing to take such affirmative steps as may be necessary to prevent the recurrence of any discriminatory conduct in the future and to eliminate to the extent practicable, the effects of Old Kent Bank and Old Kent Financial Corporation's unlawful practices; including redefining its CRA assessment area to include the City of Detroit and to service the entire delineated assessment area without regard to any prohibited characteristics, specifically including an applicant's race or the race of the area in which he or she resides or does business;

(3) Awards such actual and compensatory damages that fully compensate all the victims of Old Kent Bank and Old Kent Financial Corporation's unlawfully discriminatory policies and practices for the injuries caused by Old Kent Bank and Old Kent Financial Corporation, pursuant to 42 U.S.C. § 3614(d)(1)(B) and/or 15 U.S.C. § 1691e(h);

(4) Awards such punitive damages to all victims of Old Kent Bank and Old Kent Financial Corporation's unlawfully discriminatory policies and practices for the injuries cause by Old Kent Bank and Old Kent Financial Corporation, pursuant to 42 U.S.C. § 3614(d)(1)(B) and/or 15 U.S.C. § 1691e(h); and

(5) Assesses a civil penalty against the defendants for the actions of Old Kent Bank and Old Kent Financial Corporation in an amount authorized by 42 U.S.C. § 3614(d)(1)(C), in order to vindicate the public interest.

FURTHER, the United States prays for such additional relief as the interests of justice may require.

| JOHN ASHCROFT U.S. Attorney General | |

| _______________________ Jeffrey G. Collins United States Attorney Eastern District of Michigan U.S. Department of Justice | _________________________ R. Alexander Acosta Assistant Attorney General Civil Rights Division |

| ______________________ Pamela J. Thompson Executive Assistant U.S. Attorney Judith E. Levy Assistant U.S. Attorney Eastern District of Michigan Suite 2001 211 W. Fort St. Detroit, Michigan (313) 226-9770 | _________________________ Steven H. Rosenbaum Chief Timothy J. Moran, Deputy Chief Valerie R. O'Brian, Attorney Housing & Civil Enforcement Section - NWB Civil Right Division U.S. Department of Justice 950 Pennsylvania Avenue Washington, D.C. 20530 (202) 514-3510 |

Document Filed: May 19, 2004 > >